You’ve probably heard a lot about interest rates rising and affecting the cost of borrowing for mortgage holders over the last two years. But what exactly do higher interest rates mean for you? Read on to find out.

Borrowers benefited from more than a decade of low interest rates. Between May 2009 and April 2022, the Bank of England’s (BoE) base interest rate was below 1%, so the interest added to debts was relatively small. However, that’s now changed.

As the UK economy recovered from the Covid-19 pandemic and inflation reached a 40-year high, the BoE started to increase its base rate. As of August 2024, it stands at 5%.

As inflation fell to the BoE’s 2% target in May 2024, the BoE began to cut interest rates in August 2024. Yet, it’s very unlikely to go back to the historic lows that benefited borrowers previously.

A mortgage is often among the largest loans you’ll ever take out. So, it’s important to understand how interest rates might affect the cost of borrowing. The interest rate you’re offered could affect your outgoings now and how much your mortgage costs overall.

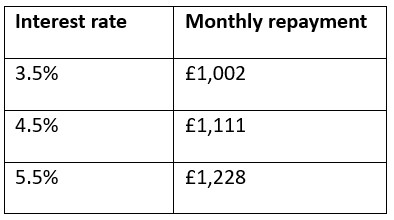

The interest rate you pay has a direct effect on your outgoings

When you take out a repayment mortgage, each month, you’ll pay the accrued interest and a portion of the amount you initially borrowed. As a result, the interest rate has a direct effect on your outgoings.

As you typically borrow large sums to buy a home, even a seemingly small change in the interest rate could have a large effect on your regular expenses.

The table below shows how your monthly repayments would change depending on the interest rate if you borrowed £200,000 through a 25-year repayment mortgage.

Source: MoneySavingExpert

In this case, a change of just 1% adds more than £100 to your mortgage outgoings. If you borrowed more through a mortgage, the difference would be even more stark.

Shopping around to find a mortgage with a lower interest rate could help reduce your day-to-day outgoings.

A higher interest rate could mean you pay thousands of pounds more over the mortgage term

It’s not just your monthly budget that’s affected by a higher interest rate. It could affect your financial future more than you expect, as you could pay significantly more over the full term of the mortgage.

Using the same scenario as above – borrowing £200,000 with a 25-year repayment mortgage – the below table shows how the total cost of borrowing is affected by the interest rate.

Source: MoneySavingExpert

As you can see, a 2% difference in the interest rate means that over 25 years, you’d pay far more in interest. That extra money could make a huge difference to your financial security or lifestyle. Perhaps you could contribute it to your pension so you’re able to retire sooner, or spend it on holidays to create memories with your family.

The good news is that there are some steps you can take to reduce how much mortgage interest you pay, including:

- Put down a larger deposit: The more equity you hold, the less of a risk you pose to lenders. So, a lender is more likely to offer you a favourable interest rate if you’re able to put down a larger deposit.

- Review your credit report: Lenders will use your credit report to assess how risky lending to you is. Taking some time to review it first could help you identify red flags and potentially fix them so lenders are more likely to offer a lower rate of interest.

- Make mortgage overpayments: If you can, overpaying your mortgage can reduce the amount of interest you pay overall. Any overpayment you make will reduce the outstanding balance and allow you to pay off your mortgage faster. Keep in mind that you may have to pay a fee when overpaying, so it’s important to check your paperwork.

- Shorten your mortgage term: How long you pay your mortgage also affects the total cost of borrowing. As a result, opting for a shorter term could save you money overall. However, it would also increase your monthly repayments.

- Work with a mortgage adviser: There are lots of mortgage deals available to choose from, and it can be difficult to know which is right for you. A mortgage adviser can review deals on your behalf and potentially secure you a better interest rate.

Get in touch if you’d like expert advice when searching for a mortgage

If you’d like to benefit from our expertise when you’re searching for a mortgage, please contact us.

We’ll take the time to understand your mortgage needs, circumstances, and priorities, so we can find a deal that suits you and could potentially help you secure a competitive interest rate that saves you money. We’ll also be on hand throughout the application process to answer your questions and offer guidance.

Please note:

This blog is for general information only and does not constitute financial advice, which should be based on your individual circumstances. The information is aimed at retail clients only.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it. Think carefully before securing debts against your home.

Production

Production